Should You Use Margin To Position Size Your Algo Strategies?

A new trader I know was lamenting about a futures algo trading system he was interested in trading. "I like it a lot," he said, "but it holds trades overnight. That means I can only trade half as many contracts, because of the exchange margin requirements. I am trying to trade as many contracts as I can, and I like the lower day trade margins."

I'm sure some of you are reading this nodding your heads in agreement. Is this sort of position sizing a problem? It sure is.

Let me put this bluntly: If you position size based on minimum margin requirements (i.e., maximize the amount of contracts or lots to trade) in ANY futures or forex market, eventually you most likely will lose all your money, because you are overtrading. Your risk of ruin becomes huge when you overtrade or overleverage.

How do I know this? 1) I've blown out accounts doing this myself, and 2) margin requirements are determined by the exchanges, which have nothing to do with your particular trading method. How can you base your position size on a number (margin required) which knows nothing about your particular potential losses and drawdowns?

So, how should you position size? There are numerous position sizing methods out there, and many good books on the topic. The key is your position sizing should reflect your tolerance for risk and reward, and should incorporate characteristics of your particular system. For example, if you knew your tolerance for maximum drawdown was 50%, you could take that requirement, combine it with your system's trade history, and run a Monte Carlo analysis to determine the appropriate position sizing technique.

Now, you might be saying "Woah...Monte Carlo testing? What's that? How do I do it?" Luckily, I have that covered for you. Head over to my Trading Calculators page, and you will find a Monte Carlo spreadsheet you can download.

Here is an example of how it works, and how you can figure out if your risk of ruin is too high.

Right now the exchange minimum margin for ES (mini S&P) is $6,930 per contract. Some brokers, however, offer what they call "day trading margin" of $500 per contract.

So, let's say you have a $750 account. To play it "safe" you will trade 1 contract ($500 margin) for every $750 in your account. If your equity ever falls below $500, you are wiped out - ruined - and you cannot trade anymore. Sound fair?

Now, let's give a positive expectancy (winning) system to trade. It trades 1 time per day, and either gains $75, or loses $60 (net after slippage and commissions). A 50% winning algo system, and on average you make $7.50 per day, and over 1 year (250) trades, it should return $1,875, a huge percentage return on a $750 account. And that is without adding on any contracts as your equity grows!

How does that look when you put it in the Monte Carlo simulator?

I'm sure some of you are reading this nodding your heads in agreement. Is this sort of position sizing a problem? It sure is.

Let me put this bluntly: If you position size based on minimum margin requirements (i.e., maximize the amount of contracts or lots to trade) in ANY futures or forex market, eventually you most likely will lose all your money, because you are overtrading. Your risk of ruin becomes huge when you overtrade or overleverage.

How do I know this? 1) I've blown out accounts doing this myself, and 2) margin requirements are determined by the exchanges, which have nothing to do with your particular trading method. How can you base your position size on a number (margin required) which knows nothing about your particular potential losses and drawdowns?

So, how should you position size? There are numerous position sizing methods out there, and many good books on the topic. The key is your position sizing should reflect your tolerance for risk and reward, and should incorporate characteristics of your particular system. For example, if you knew your tolerance for maximum drawdown was 50%, you could take that requirement, combine it with your system's trade history, and run a Monte Carlo analysis to determine the appropriate position sizing technique.

Now, you might be saying "Woah...Monte Carlo testing? What's that? How do I do it?" Luckily, I have that covered for you. Head over to my Trading Calculators page, and you will find a Monte Carlo spreadsheet you can download.

Here is an example of how it works, and how you can figure out if your risk of ruin is too high.

Right now the exchange minimum margin for ES (mini S&P) is $6,930 per contract. Some brokers, however, offer what they call "day trading margin" of $500 per contract.

So, let's say you have a $750 account. To play it "safe" you will trade 1 contract ($500 margin) for every $750 in your account. If your equity ever falls below $500, you are wiped out - ruined - and you cannot trade anymore. Sound fair?

Now, let's give a positive expectancy (winning) system to trade. It trades 1 time per day, and either gains $75, or loses $60 (net after slippage and commissions). A 50% winning algo system, and on average you make $7.50 per day, and over 1 year (250) trades, it should return $1,875, a huge percentage return on a $750 account. And that is without adding on any contracts as your equity grows!

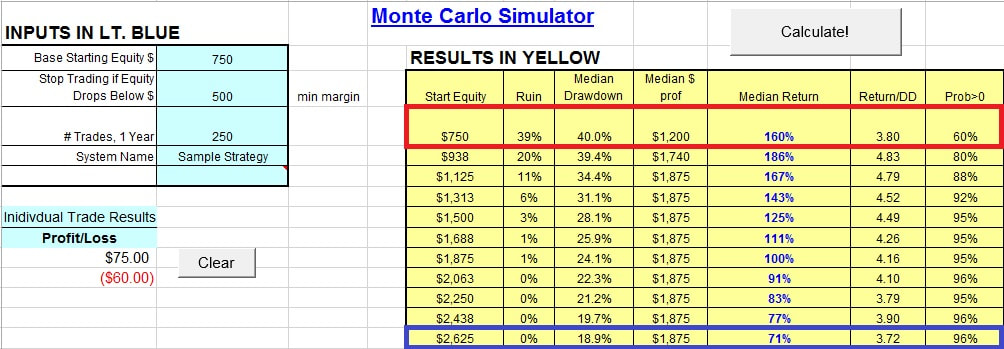

How does that look when you put it in the Monte Carlo simulator?

Take a look at the box outlined in red. Start with $750, and your risk of ruin is 39%! Yikes!!! That says, even with this positive expectancy (winning) algo system, you have a very real chance of getting wiped out during the next year.

But, if you increase your starting equity to around $2,5000 (blue box), your risk of ruin goes to almost zero!

The lesson here is that you need enough capital to weather the storms that always occur when you trade.

One key to survival I've found over the years is not to overtrade. Trying to maximize the position size based on minimum margin requirements is definitely overtrading.

But, if you increase your starting equity to around $2,5000 (blue box), your risk of ruin goes to almost zero!

The lesson here is that you need enough capital to weather the storms that always occur when you trade.

One key to survival I've found over the years is not to overtrade. Trying to maximize the position size based on minimum margin requirements is definitely overtrading.

About The Author: Kevin Davey is an award winning private futures, forex and commodities trader. He has been trading for over 25 years.Three consecutive years, Kevin achieved over 100% annual returns in a real time, real money, year long trading contest, finishing in first or second place each of those years.

Kevin is the author of the highly acclaimed book "Building Algorithmic Trading Systems: A Trader's Journey From Data Mining to Monte Carlo Simulation to Live Trading" (Wiley 2014). Kevin provides a wealth of trading information at his website: http://www.kjtradingsystems.com

Copyright, Kevin Davey and KJ Trading Systems. All Rights Reserved. Reprint of above article is permitted, as long as the About The Author information is included.

Kevin is the author of the highly acclaimed book "Building Algorithmic Trading Systems: A Trader's Journey From Data Mining to Monte Carlo Simulation to Live Trading" (Wiley 2014). Kevin provides a wealth of trading information at his website: http://www.kjtradingsystems.com

Copyright, Kevin Davey and KJ Trading Systems. All Rights Reserved. Reprint of above article is permitted, as long as the About The Author information is included.