How "Peel Off" Trading Can Lead To Improved Trading Profits

Many traders have a favorite method for trading, and they rarely deviate from that plan, regardless of what they are trading. One method many people like is what I call the “peel off” method. In its simplest form, the trader starts out with two contracts, exits the first at a small profit (the “peel off”), and then holds the second as a “runner,” going for big profits. In some cases when the first contract is exited, the second contract is then modified to have a breakeven stop.

Of course, for every person who uses this method, another person thinks the approach is complete hogwash. Personal feelings aside, I always like to do what the data tells me; if the performance improves with a certain method, then I’ll use it. If it makes it worse, I’ll discard the idea. That is what makes algo trading great - you get to test your idea or theory, and see if it actually holds water. No more guessing or using hindsight!

With that approach in mind, let’s examine the “peel off” method for a few actual trading systems.

Analysis Approach

For a first cut in the evaluation, we’ll keep things simple. First, we will run our baseline case, two contracts traded for each trade. In the second case (the “peel off” case), we will enter each trade with two contracts, and exit the first with a profit of ProfSTS dollars.

In Tradestation, assuming Condition 1 is our entry criteria, and Condition 2 is our exit criteria, the code for long entries would look like this:

Baseline Code

If Condition1 then buy 2 contracts next bar at market; If Condition2 then sell 2 contracts next bar at market;

For the “peel off” case, the code would look like this:

“Peel Off” Code

Input: ProfSTS(500); //profit threshold for exiting the first contract

If Condition1 then buy 2 contracts next bar at market;

If CurrentContracts > 0 then begin //prevents division by zero errors

If OpenPositionProfit/CurrentContracts > ProfSTS and CurrentContracts=2 then begin

Sell 1 contract next bar at market;

End;

End;

If Condition2 then sell all contracts next bar at market;

Since we are defining ProfSTS as an input, we will be able to optimize it. This might give us some insight into when the “peel off” method is superior.

Evaluation Approach

Since each new entry always starts with two contracts, we can compare the Return on Account of the two cases. Return on Account includes Net Profit and Maximum Drawdown in its calculation, so we have risk and reward covered in one number.

Test Strategies

For this evaluation, we will test three unique strategies. These are all strategies that I personally trade and were developed using my typical walk-forward analysis approach. All of the strategies are different:

Baseline Results

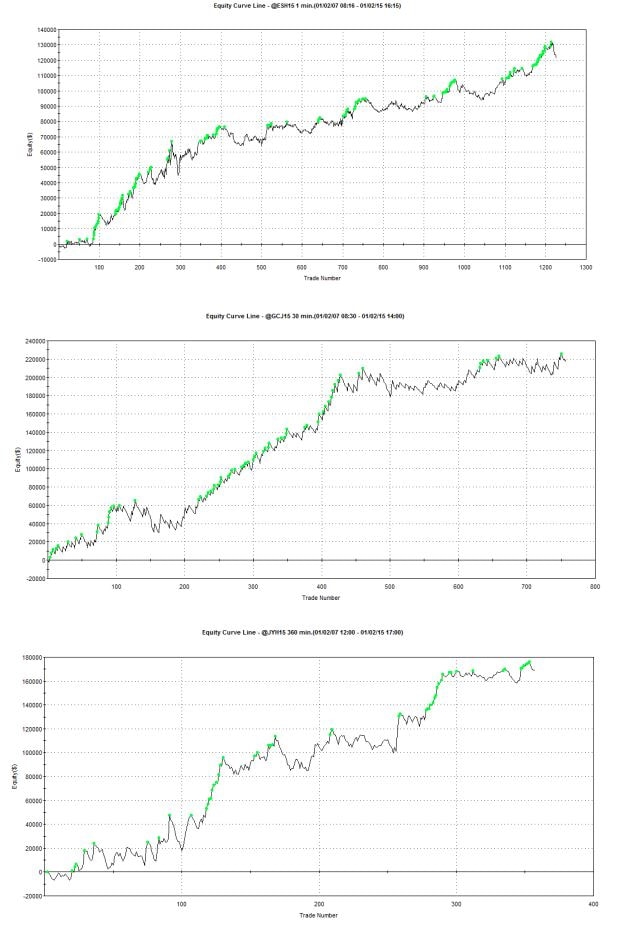

The overall walk-forward performance for each of the strategies, trading two contracts each, is shown below.

Of course, for every person who uses this method, another person thinks the approach is complete hogwash. Personal feelings aside, I always like to do what the data tells me; if the performance improves with a certain method, then I’ll use it. If it makes it worse, I’ll discard the idea. That is what makes algo trading great - you get to test your idea or theory, and see if it actually holds water. No more guessing or using hindsight!

With that approach in mind, let’s examine the “peel off” method for a few actual trading systems.

Analysis Approach

For a first cut in the evaluation, we’ll keep things simple. First, we will run our baseline case, two contracts traded for each trade. In the second case (the “peel off” case), we will enter each trade with two contracts, and exit the first with a profit of ProfSTS dollars.

In Tradestation, assuming Condition 1 is our entry criteria, and Condition 2 is our exit criteria, the code for long entries would look like this:

Baseline Code

If Condition1 then buy 2 contracts next bar at market; If Condition2 then sell 2 contracts next bar at market;

For the “peel off” case, the code would look like this:

“Peel Off” Code

Input: ProfSTS(500); //profit threshold for exiting the first contract

If Condition1 then buy 2 contracts next bar at market;

If CurrentContracts > 0 then begin //prevents division by zero errors

If OpenPositionProfit/CurrentContracts > ProfSTS and CurrentContracts=2 then begin

Sell 1 contract next bar at market;

End;

End;

If Condition2 then sell all contracts next bar at market;

Since we are defining ProfSTS as an input, we will be able to optimize it. This might give us some insight into when the “peel off” method is superior.

Evaluation Approach

Since each new entry always starts with two contracts, we can compare the Return on Account of the two cases. Return on Account includes Net Profit and Maximum Drawdown in its calculation, so we have risk and reward covered in one number.

Test Strategies

For this evaluation, we will test three unique strategies. These are all strategies that I personally trade and were developed using my typical walk-forward analysis approach. All of the strategies are different:

- An intraday 1-minute bar ES strategy that has no profit target, and a large stop loss

- A 30-minute bar Gold swing system, with both a profit target and a stop loss

- A 360-minute Japanese Yen swing system, with just a stop loss

Baseline Results

The overall walk-forward performance for each of the strategies, trading two contracts each, is shown below.

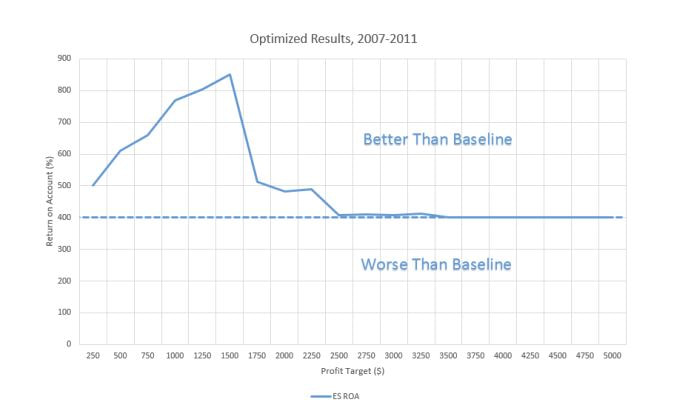

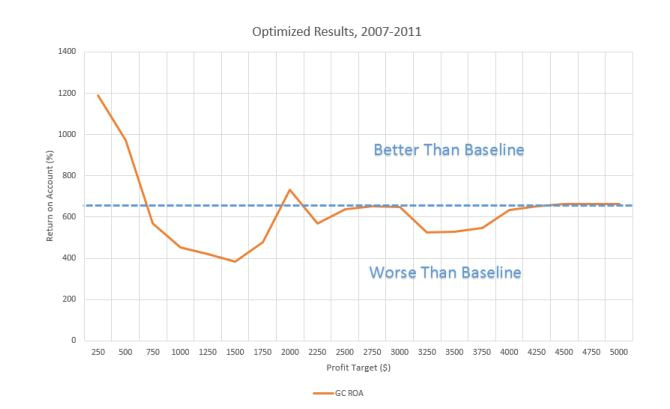

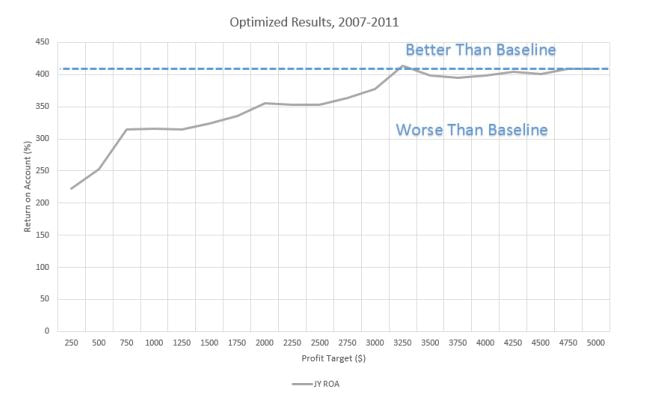

In-Sample Optimization Results

To test how the “peel off” scheme works, 5 years of data will be used to optimize the profit target exit level (input ProfSTS) and then validated on the out-of-sample data, which is a 3 year period. The optimization will use the maximum Return on Account as its criteria. (Note, for this test I am not using walkforward testing, which I highly encourage for your normal strategy development process).

Results of the in-sample optimization are shown in the charts below.

For the ES strategy, the “peel off” method always produces results as good as, or better than, the baseline case of holding two contracts throughout the trade. The maximum Return on Account corresponds to a profit target of $1,500 which produces a Return on Account more than double of the baseline case.

To test how the “peel off” scheme works, 5 years of data will be used to optimize the profit target exit level (input ProfSTS) and then validated on the out-of-sample data, which is a 3 year period. The optimization will use the maximum Return on Account as its criteria. (Note, for this test I am not using walkforward testing, which I highly encourage for your normal strategy development process).

Results of the in-sample optimization are shown in the charts below.

For the ES strategy, the “peel off” method always produces results as good as, or better than, the baseline case of holding two contracts throughout the trade. The maximum Return on Account corresponds to a profit target of $1,500 which produces a Return on Account more than double of the baseline case.

For the GC strategy, sometimes the “peel off” method is better, and sometimes it is not. Based on the optimization, we will use a profit target of $250 which produces nearly double the Return on Account, compared to the baseline.

For JY, the “peel off” method is almost always worse than the baseline case. Its optimum is at $3,250 profit level.

Verification With Out-Of-Sample Results

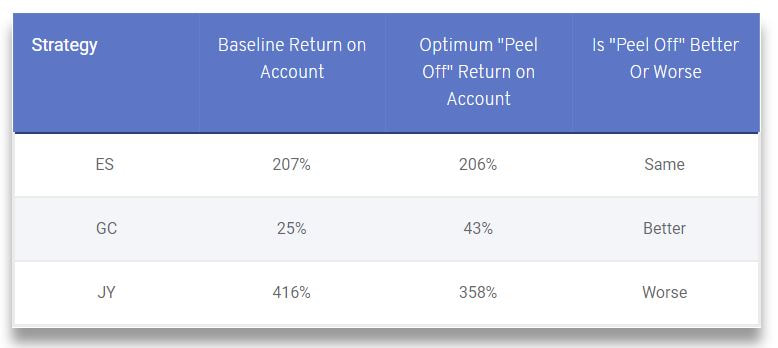

Now that we have established the optimum profit target to “peel off” the first contract, we can run the results on out-of-sample data for 3 years. These results are shown in the table below.

Now that we have established the optimum profit target to “peel off” the first contract, we can run the results on out-of-sample data for 3 years. These results are shown in the table below.

Results of the out-of-sample analysis are mixed. The ES is the same, the GC strategy is better with the “peel off” method, and the JY strategy is better with the baseline (always trading two contracts).

Major Problem With This Analysis

While this analysis was inconclusive – sometimes the “peel off” method was better, sometimes it was worse, it should be noted that implementing a major strategy change like this, in general, should not be done once the strategy is complete. In this study, I took existing strategies, developed, and optimized without the “peel off” method in mind – and then added on the “peel off” approach. Clearly, this is not the best way to do it. I did it for this study because I primarily wanted to show the “peel off” approach on actual live trading strategies.

The correct way to build a strategy with “peel off” is to include the rule at the start of development. That way, the whole strategy is optimized with “peel off” in mind. If it improves the performance, then it will be in the strategy from the beginning, rather than bolted on at the end. This is a much more preferable way of developing – since adding on rules, etc. after development can easily lead to curve fitting (the old problem of continuously trying to improve backtest results).

Conclusion

This article has demonstrated how to analyze the performance of the “peel off” method of trading, where one contract is exited at a smaller profit, and a second contract is allowed to run. Not surprisingly, different strategies yield different conclusions about “peel off” trading, although some of that may be due to the analysis method itself (evaluating the method on an existing strategy).

It is recommended that the reader, if he possibly wants to include the “peel off” method, incorporate the approach at the very beginning of strategy development and analysis, and utilize a robust walk-forward test process to analyze the strategy.

Major Problem With This Analysis

While this analysis was inconclusive – sometimes the “peel off” method was better, sometimes it was worse, it should be noted that implementing a major strategy change like this, in general, should not be done once the strategy is complete. In this study, I took existing strategies, developed, and optimized without the “peel off” method in mind – and then added on the “peel off” approach. Clearly, this is not the best way to do it. I did it for this study because I primarily wanted to show the “peel off” approach on actual live trading strategies.

The correct way to build a strategy with “peel off” is to include the rule at the start of development. That way, the whole strategy is optimized with “peel off” in mind. If it improves the performance, then it will be in the strategy from the beginning, rather than bolted on at the end. This is a much more preferable way of developing – since adding on rules, etc. after development can easily lead to curve fitting (the old problem of continuously trying to improve backtest results).

Conclusion

This article has demonstrated how to analyze the performance of the “peel off” method of trading, where one contract is exited at a smaller profit, and a second contract is allowed to run. Not surprisingly, different strategies yield different conclusions about “peel off” trading, although some of that may be due to the analysis method itself (evaluating the method on an existing strategy).

It is recommended that the reader, if he possibly wants to include the “peel off” method, incorporate the approach at the very beginning of strategy development and analysis, and utilize a robust walk-forward test process to analyze the strategy.

About The Author: Kevin Davey is an award winning private futures, forex and commodities trader. He has been trading for over 25 years.Three consecutive years, Kevin achieved over 100% annual returns in a real time, real money, year long trading contest, finishing in first or second place each of those years.

Kevin is the author of the highly acclaimed book "Building Algorithmic Trading Systems: A Trader's Journey From Data Mining to Monte Carlo Simulation to Live Trading" (Wiley 2014). Kevin provides a wealth of trading information at his website: https://kjtradingsystems.com

Copyright, Kevin Davey and KJ Trading Systems. All Rights Reserved. Reprint of above article is permitted, as long as the About The Author information is included.

Kevin is the author of the highly acclaimed book "Building Algorithmic Trading Systems: A Trader's Journey From Data Mining to Monte Carlo Simulation to Live Trading" (Wiley 2014). Kevin provides a wealth of trading information at his website: https://kjtradingsystems.com

Copyright, Kevin Davey and KJ Trading Systems. All Rights Reserved. Reprint of above article is permitted, as long as the About The Author information is included.