How To Bring Your Algo Trading to the Next Level

Most new traders take up mechanical or algo trading with one thought in mind: to historically test their trading idea or strategy in order to “prove” it works. Most trading software is built around this objective. Simply pull up a chart, insert a strategy, quickly run hundreds, thousands or millions of optimization runs, and review the best results. The best parameter set is then used in live trading.

Algorithmic Trading Ideas

Alas, if the process was only so easy! The reality is that the simple approach – the method that most software encourages – is also the method least likely to work in the future. The old computer adage “garbage in, garbage out” certainly applies here. Traders who have a “garbage” development process will typically receive “garbage” from the testing software - a strategy that performs poorly in real time.

The solution is to build a strategy with the right process. But what is right, and what is wrong? This article examines some different development decisions that need to be made, and can be a guide to some best development practices.

Start With An Idea

Regardless how a strategy is evaluated, every trading strategy starts with an idea. So that is where we will start. Just as there are good and bad ways to test, which will be discussed later, there are also good and bad sources of trading ideas, as shown in Table 1. Here we highlight a few:

Trading Idea Resources

Books/Magazines/Internet Sites

There are literally thousands of public domain sources for algo trading ideas. These could be fully defined strategies, or just strategy components, such as entries and exits. The problem is that these public domain sources rarely work well as is. Think about it – why would someone knowingly disclose a superb trading system or idea, instead of keeping it secret and just trading it for themselves? Most sane traders would keep it secret. This means that most of the public domain ideas will not perform well when tested. But, that does not imply they are worthless.

Public sources of ideas can be a terrific place to start a trading strategy. Simply taking ideas/code and modifying it to make it unique is a very common technique used by experienced developers. They rely on the public domain for the “seed” idea, but the trader then takes the idea and grows it.

Here is an example of a good article for trading ideas, specifically about exits.

Random ideas

There are a few software products out there that will randomly take trading ideas and test them out, via machine learning, artificial intelligence or genetic optimization. Typically, millions of different trading strategies are created, and the best performing one is selected. While on the surface this seems reasonable, the same issues of over-optimization that plague a single multi-variable system are likely to negatively impact a randomly generated strategy.

If a few million trading strategies are generated, chances are at least a few will perform well, and that could all be due to chance. While it is possible to randomly discover an edge, it is far easier to randomly discover a fluke strategy that just happens to test well.

Trader experience

An excellent source of trading ideas comes from a trader’s own experience. What could be better than continually observing some market pattern, and then turning it into a successful strategy? While this sounds great in theory, reality is a little tougher. What frequently looks like predictable behavior on a chart or two turns out to be a short lived anomaly.

Of course, rigorous testing will reveal that, but many traders develop an idea based on a very limited sample of charts, quickly evaluate it and then begin to trade it. This almost never works. Good traders, though, will combine their experience with proper testing, and can frequently build good trading strategies because of it.

Turning an Idea Into a Strategy

Once the idea is formed, most traders will typically do one of two things with it: keep the number of rules and conditions small, or add a multitude of filters, conditions and rules to entries and exits to improve the strategy performance. Both approaches have their pros and cons.

Very Few Rules

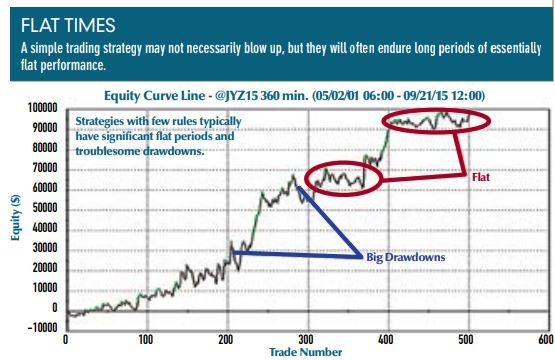

Many traders espouse the theory that “simplest works best.” This definitely can be true in real time trading. The problem is that simple trading ideas yield imperfect results – large and significant drawdowns and periods of flat and generally unremarkable performance are the norm, such as the strategy results for a simple strategy shown in the figure below.

Paranoid traders worry about someone else determining their simple rules, and since thousands of people are out there every day building systems, it makes sense that the simpler ideas will be discovered first. So, quite a few traders dismiss the simple ideas in favor of strategies with many rules and conditions.

Lots of rules

The flip side to minimal rule strategies is a strategy with dozens of rules, parameters and conditions. Typically, these systems will be adjusted every time a big loss is encountered – in effect, engineering losses out of the backtest. Equity curves produced with complicated systems typically have a very appealing historical backtest.

The problem with such strategies, obviously, is that markets change; future losses will likely be slightly different than historical losses, and any attempt to circumvent these losses really will only yield a more unrealistic backtest. Future performance usually suffers as more rules are added, which many find hard to accept.

Time period to test

Once the core strategy is established, traders have to decide what time period to test it on. While some of this decision will be influenced by the testing method (see below), there are always a few key points to consider:

- More history is better than less history. Given a choice between historical testing for one year, and ten years, the choice should be clear: more history is better, since it means more trades, and more unique market conditions and phases to evaluate the strategy over.

- Finding strategies that work 5-10 years of data is much more difficult than finding a one month super performer. Traders need to resist the urge to go with the easy testing, and instead test of more data.

- Most data providers do not provide unlimited tick data history. Many vendors only provide 6 months of tick data. This rules out a long backtest. Therefore, tick data should be used with extreme caution, or ideally not at all.

- Besides the limited amount of tick data available, historical tick data is sometimes filtered and aggregated by the exchange or data provider. This could lead to misleading historical results, as the data today might be significantly different than data of a few years ago.

Algorithmic Trade Testing

On To Testing

The type of testing performed can have a serious impact on creating good strategies. Here is a discussion of 4 major types of testing.

Traditional Backtest

As mentioned earlier, trading software promotes a traditional backtest where all the data is analyzed and rules optimized based on the whole dataset. The problem is that, just like with randomly generated trading ideas, a few iterations out of a few thousand iterations will always be superb looking. But, that does not mean that the strategy will actually work well going forward.

Out Of Sample Testing

This approach takes a traditional backtest, optimizes over 80% of the data (“In sample”), and evaluates that 20% (“out of sample”) based on the best optimization results of the 80% of data. This is much better than traditional optimizing, although the tendency to test and retest still exists, which can easily transform the out of sample period into an in sample period. Also, the parameters would never change with time or with market conditions. This can be a problem that walkforward testing can remedy.

Walkforward Testing

Considered the best test method by many, walkforward testing combines multiple out of sample history pieces to create a longer term, out of sample performance curve. In this respect, it is clearly better than a single out of sample test. But, this method is more complicated, and tougher for most traders to understand. Therefore, many shy away from it. Many experienced traders, though, agree that walkforward testing is the next best thing to live trading.

Live Testing

Every trader should agree that live testing is the ultimate judge of a strategy’s viability. Historical performance is nice to have, but live trading in a real account is the only absolute “truth” in strategy testing. In fact, more than a few traders only test in this manner – they evaluate strategies with real money, in real trading. This can be expensive, of course, especially for novice traders without any market knowledge or experience, as they test multiple bad ideas with real money. Experienced veterans are the group of traders most likely to benefit from this test method.

Conclusion

Although algorithmic and mechanical testing seems straightforward – simply program rules, test results and make an acceptance decision –there are many nuances and pitfalls to this type of trading. Traders would be well advised to research the whole field of algorithmic trading carefully before embarking on strategy development. Mistakes avoided due to a good development process can and will save thousands down the road.

About The Author: Kevin Davey is an award winning private futures, forex and commodities trader. He has been trading for over 25 years. Three consecutive years, Kevin achieved over 100% annual returns in a real time, real money, year long trading contest, finishing in first or second place each of those years.

Kevin is the author of the highly acclaimed book "Building Algorithmic Trading Systems: A Trader's Journey From Data Mining to Monte Carlo Simulation to Live Trading" (Wiley 2014). Kevin provides a wealth of trading information at his website: https://kjtradingsystems.com

Copyright, Kevin Davey and KJ Trading Systems. All Rights Reserved. Reprint of above article is permitted, as long as the About The Author information is included

.Cover photo: https://lmmediate.net/

Kevin is the author of the highly acclaimed book "Building Algorithmic Trading Systems: A Trader's Journey From Data Mining to Monte Carlo Simulation to Live Trading" (Wiley 2014). Kevin provides a wealth of trading information at his website: https://kjtradingsystems.com

Copyright, Kevin Davey and KJ Trading Systems. All Rights Reserved. Reprint of above article is permitted, as long as the About The Author information is included

.Cover photo: https://lmmediate.net/